Macro Thoughts

Thought to ponder…

“… the world of economics, business and finance is ‘non-stationary’ – it is not governed by unchanging scientific laws. Most important challenges in these worlds are unique events, so intelligent responses are inevitably judgements which reflect an interpretation of a particular situation. Different individuals and groups will make different assessments and arrive at different decisions, and often there will be no objectively right answer, either before or after the event. And because what we observe is not the outcome of a stationary process, conventional statistical inference rarely applies and forecasts are often based on shifting sands.

John Kay and Mervyn King

Radical Uncertainty

The View from 30,000 feet

This will be our final publication of Macro Thoughts for the year, with regular weekly pieces resuming January 8th. It seems only fitting that with our last Macro Thoughts of the year that the Fed should be so kind as to provide us with an exclamation mark on the year. Although Powell stopped short of taking a full victory lap on Wednesday, because inflation is still coursing through the veins of the economy, the tone of the statement and pressor took a dramatic shift. The markets, who have been impatiently waiting for this moment all year, erupted with a 9:1 advances vs. decliners day, over 70% of the S&P500 hitting new 21-day highs, and 87% of the S&P500 trading over their 50-day moving average. This type of internal thrust solidifies positive sentiment, but also puts the markets in a dangerously overbought condition. This is the 6th time since the end of the pandemic that the markets have reached this level of over bought. The last three instances of extreme overbought conditions, which all occurred since the beginning of 2022, were each followed by selloffs, whereas the previous three instances between 2020 and 2021, each marked the continuation of an uptrend. Which will this be? The answer lies with data. If the disinflationary trends persists, while the labor markets and spending remain resilient, further embedding the soft-land narrative, there is nothing in the way for the markets to churn higher. However, of the data comes in challenging the soft-landing narrative, investor conviction will wane, and markets may struggle to find footing.

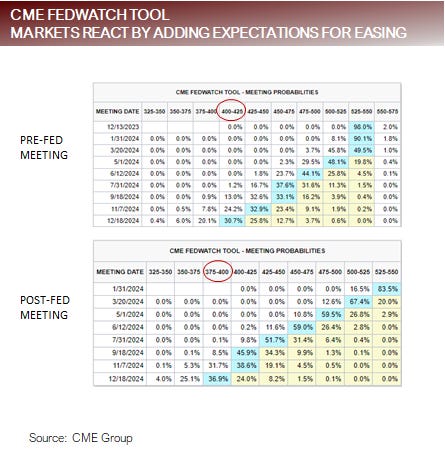

Fed changes course and the markets applaud

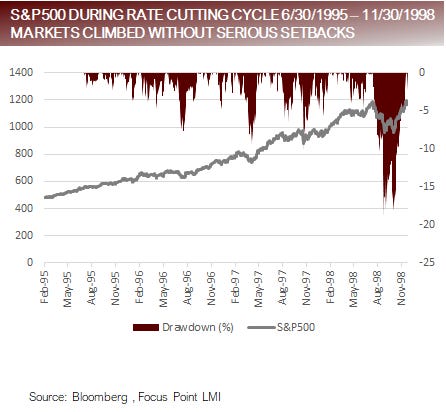

Pause – Check; Cuts expected to come next, how the markets have historically performed during cutting cycles

Republishing 2024 Outlook and looking at what’s changed since it was originally published

The most Frequently Asked Question from clients this week: What did strategists got wrong in 2023 and how do we avoid the same mistakes in 2024?

Fed changes course and the markets applaud

The prepared opening statement of the Federal Reserve’s statement follows a formula.

The first sentence is about growth.

The second sentence is about jobs.

The third sentence is about inflation.

By the time the Fed reached the third sentence of their speech on Wednesday, we knew something had changed in their assessment.

In the first sentence, there was an acknowledgement that “economic activity has slowed”.

In the third sentence, they gave the nod that “inflation has eased over the past year”.

In the prepared statements that Fed went onto augment references for raising rates by adding “any” as a qualifier to their questioning for additional firming.

The Fed also eliminated the final rate cut in 2023 and added one more cut in 2024 to the SEP, which amounted to two additional rate reductions over previous estimates, while reducing inflation estimates in the SEP for the first time in 2023.

The speech represented a U-turn from the speech Powell gave less than two weeks ago when he indicated that it was premature to think that the Fed is restrictive enough.

Durning the Q&A Powell went on to say he expected real rates to fall next year, which implies rate cuts will be in excess of those needed to move down in lock step with disinflation. This was taken be extremely dovish.

It should be noted regional Fed leadership is out in full force trying to cool sentiment and walk back the dovish tone set last week. On Friday, Williams, and over the weekend, Goolsbee and Bostic, all tried dissuade market expectations for cuts.

Early cycle sectors rally as an additional rate cut priced in for 2024

Cuts expected to come next, how the markets have historically performed during cutting cycles

We looked back to 1989, a period that covered five rate cutting cycles. It should be noted, that there are far too few data points for the data to be statistically significant, so rather than look at the data as having any forecasting ability, we simply tried to see if there were any trends worth noting.

Observations

There is a very small group to look at in the first place, but the 2019 cycle should be completely thrown out because the effects of the pandemic, related economic on/off, fiscal and monetary response make that cycle unusable for comparison.

Since the 1990’s the cycles have become increasingly shorter with larger drawdowns.

Since 2000, the lower bound for rates has been essentially zero. It’s hard to make a case that we’ll see this again, but the answer to that all hinges on inflation. Almost no one expected inflation to crest 9% on the upside, and very few are expecting to economy to return to outright deflation, but there is not a zero probability that it could happen.

In the 1990’s the S&P500 rallied through the interest rates cutting cycle with a reasonably small drawdown, but in the 2000’s the experience has been that the S&P500 experienced sharp selloffs and did not recover during the interest rate cutting cycle.

Markets hoping for a 1995 style outcome to the cycle, not at 2000 type outcome

Republishing 2024 Outlook and looking at what’s changed since it was originally published

SURPRISE RESILIENCY PROBABILITY 10%

Economy plows ahead at higher than potential, spurred by rising real wages, higher interest payments on freshly minted debt filtering through to debt holders, as well as continued fiscal spending driven by post-pandemic congressional measures and election year antics. Economic strength allows companies to exceed earnings expectations, as margins improve due to disinflation in cost structures. A better-than-expected economy supports the labor market and is paired with steady disinflation in goods that spreads to services, allowing the Fed to slowly easy, supporting multiple expansion.

SOFT-LANDING PROBABILITY 40%

The Goldilocks scenario. Disinflation in housing and autos, as well as goods in general, continues to feed disinflationary pressures. Oil prices stay under control, causing stability on the energy side of prices. As inflation comes down, real rates drift higher, compelling the Fed to lower rates to recalibrate the policy environment from becoming even more restrictive. Growth slows to slightly below trend and the labor market continues to rebalance at a controlled pace. The balance between lower rates and relative stability in the employment market allows companies to achieve earnings projections, supporting equity appreciation.

STICKY INFLATION PROBABILITY 10%

Inflation either levels off in an area slightly above the Fed’s comfort level or reaccelerates. The Fed contemplates hiking rates further, causing rates to drift higher and igniting losses on the fixed income side of portfolios. Equities begin to feel the lagging effect of higher rates as more companies and consumers are forced to refinance at higher rates. Companies and consumers with the strongest Balance Sheets are relatively unaffected, allowing spending to be sustained and because spending is in nominal dollars, earnings are maintained, while lower income groups and companies with we Balance Sheets flounder.

NOT SO SOFT-LANDING PROBABILITY 30%

The employment market deteriorates faster than expected, creating a feedback loop where consumers have less confidence and reduce spending, which leads to a markdown in corporate earnings. Falling earnings creates a repricing of equities lower. The softening labor market and falling assets prices tips the scale for the Fed from being focused on price stability to being focused on full employment, allowing them to quickly move into action, cutting rates by over 300 bps to try and get rates back in the neutral range to stabilize the markets. Equities respond to lower rates by rallying and ending the year on a higher note.

CRASH LANDING PROBABILITY 10%

The faster deterioration in the employment market is accompanied by asset price uncertainty related to commercial real estate and low-quality corporate debt. Uncertainty feeds on itself, creating lower consumer and corporate spending, larger than expected layoffs, forcing homeowners back on the market and increasing existing home inventories to levels where they are unable to clear and prices on the residential side begin to fall as well. Prompted by an icing over in the credit markets and falling asset prices, The Fed is forced to act aggressively, dropping interest rates below the neutral rate, cutting rates by as much as 400 bps and reinstating QE programs. This creates a dramatic pothole, characterized by a sharp selloff and then a V shaped rally.

Probabilities migrate with data and policy

Over the last two weeks the major developments have been:

Strength in the labor market has persisted

Initial jobless claims, continuing jobless claims and nonfarm payrolls have all shown resiliency

Growth has remained buoyant

Retail sales continue surprise on the upside

Atlanta Fed GDPNow Q4 GDP projections have increased from 1.2% at the beginning of December to 2.6% last week

Inflation continues to trend lower

CPI, PPI and the inflation expectations surveys from the University of Michigan and the New York Fed have all provided signs of that disinflation trends are in place and inflation expectations remains moored

Fed policy has come the way of the markets, with rhetoric softening and expectations for an easing of restrictive policy

The last two weeks provides a good example of how data and policy can combine to shift the probable outcome towards one end or another of the probability spectrum provided in our 2024 outlook. Based on the last two weeks, the outcomes are now more strongly favoring the Surprise Resiliency or Soft-Landing outcomes. However, it’s important to keep in mind, we’re looking at only two weeks of additional data, so don’t get too excited. Anecdotally, Goldman Sachs has now raised their 2024 S&P500 price forecast twice in the last four weeks.

FAQ: What did strategists got wrong in 2023 and how do we avoid the same mistakes in 2024?

Coming into 2023 strategists were focused on economic indicators that have historically had a high probability of forecasting recessions. Such as:

The yield curve

Interest rate policy

Manufacturing demand

Survey data

What strategists got wrong

As Powell alluded to during the most recent press conference, the dynamics driving inflation appear to have been different. Inflation was enforced by two factors where great progress has been made in 2023: Supply Chains and Labor Force Participation.

The Artificial Intelligence theme, kept the S&P500 from deteriorating under otherwise downward pressure.

When the economy reopened there was too much demand for goods, leading to goods inflation that has since transitioned to disinflation. As the reopening progressed and the demand for goods fell, a pothole in goods which looked recessionary, was more than filled with demand for services, which has remained persistent due to pent up demand and cultural changes since the pandemic.

Government sponsored pandemic relief programs flooded consumer accounts with cash that sustained spending.

Signs of strain and looming crisis in the economy and financial system were met with decisive policy action, including draining of the Strategic Petroleum Reserve, Bank Term Funding Program, use of the Treasury General Account, the Inflation Reduction Act and Employee Retention Tax Credits.

How can strategists be better in 2024, in one word: Humility

Strategists (myself included) have realized that the effects of the pandemic, the historic programs designed to stave of economic collapse of the economy, social and cultural changes in the post-pandemic world, the impacts of AI and the transitioning to a multipolar geopolitical framework with less stability have combined to made forecasting the markets with certainty more complex.

Strategists were fooled in 2023 by indicators that have historically led downturns

Putting it all together

The downtrend in inflation combined with resiliency in labor market, consumer spending and economic growth have continued to surprise on the upside, opening the door for the Fed to communicate they intend to move to a more neutral stance in the coming year, which has set off a rally in both risk assets and non-risk assets that looks sustainable as long as the data persists to enforce the narrative, but the markets are overbought and vulnerable to data disappointments.

Active managers have had to eat some humble pie in 2023 (according to FundStrat only 35% of large cap active managers are outperforming their benchmark this year) largely because the confluence of drivers from the whirlwind of post-pandemic policies, AI gaining traction in businesses and as an investment theme and the impacts realities associated with a multipolar world and what that mean for the global peace the western world had been accustomed to.

Peering into 2024, certainty has been replaced with uncertainty, identifying potential outcomes and probabilities. How exactly 2024 plays out will be impacted by the outcome of unanswered questions such as:

How long will excess savings continue to support consumer spending?

Will S&P500 companies be able to deliver on the lofty 11.5% earnings growth expectations set by analysts for 2024?

Will the labor market deteriorate and form a feedback loop with consumer spending that leads to a non-linear move in unemployment?

What will happen to the housing market if supply loosens from either lower rates (good) or a softer employment market (bad)?

Where is the tipping point when enough borrowers are forced to refinance at higher rates that there is a material impact to spending?

What is the limit on the fiscal irresponsibility of the US Congress and lenders willingness to condone it?

Will AI speculation drive a historic investment cycle and evolution in how work is done (increased productivity)?

How will the Fed react if the disinflationary trend subsides, and inflation becomes more volatile?

Will the commercial real estate market in the US enter nuclear winter and take regional banks with it?

Will the geopolitical disruptions in Europe and the Middle East spillover to hampering supply chains?

Will the Fed, Congress and the Administration be able to successfully fend off recessionary pressures with programs as the did in 2023?

What will the market reaction be to the US election?