Macro Thoughts

Thought to ponder…

“If you think about it, it’s precisely because people are different from others that they’re able to create their own independent selves. Take me as an example. It’s precisely my ability to detect some aspects of a scene that other people can’t, to feel differently than others and choose words that differ from theirs, that’s allowed me to write stories that are mine alone. And because of this we have the extraordinary situation in which quite a few people read what I’ve written. So the fact that I’m me and no one else is one of my greatest assets. Emotional hurt is the price a person has to pay in order to be independent.

Haruki Murakami and Philip Gabriel

What I Talk About When I Talk About Running

The View from 30,000 feet

Market reactions to data releases last week were centered around the labor market. JOLTS, ISM employment trends and the nonfarm payrolls all continued to support the narrative that the labor market is healthy and moving toward balance. Outside of labor market data, attention was focused on the coming week’s expected CPI release and the Fed’s meeting. With the median analyst estimate for next week’s CPI release signaling a non-existent 0.0% month-over-month increase, the soft-landing cheer squad is out in full force. Based on the disinflationary tailwinds and signs of cooling the labor markets, expectations are that the Fed will to begin to telegraph rate cuts for 2024 to keep real rates from drifting higher as inflation falls. Whether Powell plays ball with the markets will determine the tone next week. Assuming inflation stays on its current trajectory, developments in the labor market will hold the key to how quickly rates move. Think of the labor market as an amplifier, acting to increase or decrease the speed of rate cuts as inflation falls. To the degree the labor market remains strong, the Fed is likely to question if rates are restrictive enough and may resist cutting rates. Conversely, if the labor market deteriorates, combined with falling inflation, the Fed will likely be forced to act quickly to change momentum. It’s worth being aware, the consensus call for 2024 has crowded into the soft-landing camp in much the same way that the consensus crowded into the recession camp a year ago. This reminds me of an old saying – when everyone is thinking the same thing, someone isn’t thinking. Consensus thinking has an eerie way of not playing out as people think.

A rundown of labor market data last week

S&P500 top-down versus bottom-up analyst forecast point to a weak 2024 for equities

Inflation expectations, feeding off of healing supply chains and commodity prices, begin to plummet

The most Frequently Asked Question from clients this week: Does Fed interest rate policy matter?

A rundown of labor market data last week

Last week’s labor market report could be summarized as, there is a slowing of demand for workers, but companies are not aggressively reducing the size of their labor force. This is precisely what the Fed would like to see because it would represent a cooling in economic growth to below trend, without a contraction in the economy – the narrow path to a soft-landing.

JOLTS

Job Openings fell to 8733k, with the prior month revised 200k lower. The current Job Openings level is still elevated about 1m above the pre-pandemic norm, but the job openings to unemployed workers ratio fell to 1.3x after cresting 2.0x at its high and is closing in on the pre-pandemic norm of 1.0x.

The Quits Rate, which closely tracks wage increases, stayed at post-pandemic low of 2.3%, which is consistent with pre-pandemic norms.

ISM

The ISM Services Employment component disappointed to the downside and confirmed the trend in last week’s Manufacturing Employment component release. Both Service and Manufacturing companies are reporting less demand for workers.

Nonfarm Payrolls

A mostly positive note, the Unemployment rate unexpected decreased to 3.7% from 3.9%, the number of nonfarm payrolls increased 199k, above estimates, and Average Weekly Hours increased, with a slight uptick in Labor Participation.

Positive labor news strikes mild fear into the soft-landing cheer squad because it may lead the Fed to be resistant to rate cuts.

Between the lines, it was possible to make a less positive case about the numbers because there was a lot of noise in the data due to the UAW strike. Additionally, economically sensitive areas and leading indicators of employment embedded in nonfarm payrolls didn’t participate at levels consistent with a solid labor market, so the data could be interpreted less optimistically, in support of a cooling labor

Normalizing and deteriorating are the two operative words to describe the workforce

S&P500 top-down versus bottom-up analyst forecast point to a weak 2024 for equities

Top-Down

The Bloomberg survey of strategist includes forecasts for the S&P500 for 2024 from 13 analysts. The average analyst forecast for the S&P500 for 2024 is 4,723.08, which represent an upside of 2.6% over Friday’s close.

According to the same survey, 19 analysts have provided S&P500 earnings forecasts for 2024, the average of which is $230.32, which would represent an increase of 4.2%

Bottom-up

The Factset bottom-up S&P500 closing target for 2024, which can be calculated by aggregating the median price target of each of the constitutes, is 5,068.41, which would represent a 10.5% increase over Friday’s close.

However, bottom-up price targets have historically overestimated market performance. In fact, according to Factset, over the last 20 years (2003 to 2022), the average overestimate using bottom-up aggregation is 7.2%.

If the average overestimation is subtracted from the bottom-up aggregation, the Factset bottom-up S&P500 closing target for 2024 is also up 2.6% from Friday’s close, exactly matching the top-down strategists.

The Factset bottom-up S&P500 earnings for 2024 are forecast is currently $246.36, up an expected 11.5%

Observations about the similarities and differences

Both the top-down and bottom-up land on the same forecast for price appreciation for 2024, an anemic 2.6% increase. However, the bottom-up analyst get there with an expectation of 11.5% earnings growth, where the top-down expect 4.2% earnings growth. Given that bottom-up analysts tend to overestimate earnings forecasts and reduce their estimates as the year progresses, it’s likely their number will come the way of the top-down strategist.

The curious thing about both forecasts is that if a soft-landing is the consensus, characterized by continued growth, a resilient labor market and lower interest rates, how does this formula equate to a stock market that is essentially flat for 2024?

One of the central questions of 2024 is if companies can deliver on lofty expectations

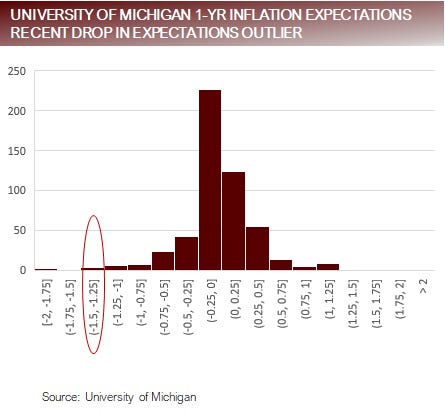

Inflation expectations, feeding off of healing supply chains and commodity prices, begin to plummet

The University of Michigan 1-Yr Inflation Expectations dropped from 4.5% to 3.1%, far undershooting the expectation of 4.3%. To put this in perspective, the one-month decline in inflation expectations of -1.4%, is in the top three largest declines since 1980, with the only two periods having larger drops being during the recessions in 1981 and 2001.

The Bloomberg Commodity Index, which tracks 23 commodities, is currently down -13.25% year-to-date, with only four constituents turning in a positive year. If the year were to end today, this would be the 9th worst year since 1960.

The Federal Reserve Bank of New York Supply Chain Pressure Index has recently recovered to measure within the range of the last decade after falling to an all-time low at the end of May this year.

Gasoline futures have collapsed from a high of 296 in August, falling to 205 as of the close Friday, down -31%. The average cost of gallon of gasoline in the US has similarly fallen from 3.88 in September to 3.16, as of Friday, down -19%. The fall in energy prices has sent OPEC+ scrambling to cut production to shore up prices.

After peaking at 10377 during the pandemic, the WCI Composite Container Freight Benchmark, has now fallen to 1461, approximately 7% lower than before the pandemic, and -32% lower than where it began the year.

Bottom Line

The commodity complex and supply chains have moved from disinflation to outright deflation. Lower prices are beginning to trickle down to the consumer through lower prices of goods and, in your face billboards that broadcast inflation to consumers, like gasoline. This is has caused inflation expectations to fall at a pace not seen in the past outside recessions.

The recent drop in gasoline prices has driven inflation expectations sharply lower

FAQ: Does Fed interest rate policy matter?

An interesting point that’s been floating around as an observation recently is that the Fed raised rates from 0.25 in March 2022 to 5.50 in July of 2023, and there seems to have been no impact to growth or the employment market (based on unemployment or jobless claims). So, does raising interest rates really work to cool the economy?

Yes, raising interest rates does matter. The question is, to whom? Interest rates were extreme low coming into hiking cycle, allowing investors who has access to credit the ability to term out their debt. It seems the only borrower who didn’t take advantage of terming out their debt was the US government, who is now facing $8t of refinancing needs in 2024.

Looking at the subprime auto market there is evidence of what happened to borrowers who couldn’t term out their debt and are forced to pay market rates. According to Fitch subprime 60 day plus delinquencies are at an all-time high going back to the beginning of the index in 1991.

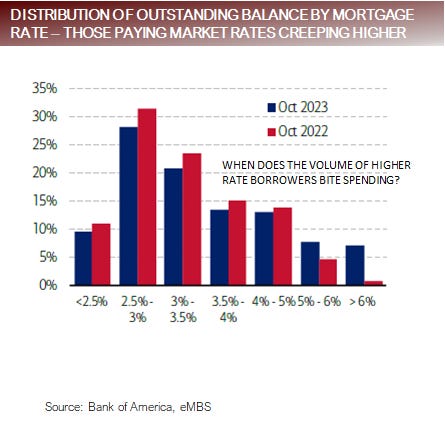

The impact of terming out debt is going to last forever. Bank of America published a research piece recently where they noted that eMBS data shows that in October 2022 over 80% of mortgages had a rate of less than 4%, but by October 2023, that number had dropped to 72%. About 8% of mortgage holders required financing last year, being forced to pay higher rates.

Similarly, Goldman Sachs recently estimated that the average interest rate of long-term debt for the S&P500 is 3.2%, and that about 8% of that debt will mature next year, which will require the new debt to be financed at market rates.

Borrowers who couldn’t term out their debt are being impacted. Ask the US government how that’s going. The question is, when are enough of the borrowers forced into the market to finance that it will cause trauma that it trickles through to lower spending? In 2023 excess saving may have obfuscated the answer to this question but that could change in 2024.

Higher interest rates matter to borrowers with no other choice but to borrow today

Putting it all together

A soft-landing is the consensus call for 2024. Many of those who called for a recession in 2023, have now reluctantly hopped onboard the soft-landing train, while those who called for positive markets in 2023 are doubling down in 2024.

We’re always nervous when everyone starts to lean to one side of the boat. In hindsight, this is one of the lessons we should have all taken away from the recession call that most strategists were making at the beginning of 2023.

As we noted last week in our 2024 Outlook Macro Thoughts, we see an array of potential outcomes in 2024, with the risks skewed to the downside, but multiple scenarios that may also lead to very good outcomes for equities.

There are a lot of unknows that we’ll have to face in the coming year that will impact the probability of a soft-landing. A few of these unknowns include:

How long will excess savings continue to support consumer spending?

Will S&P500 companies be able to deliver on the lofty 11.5% earnings growth expectations set by analysts for 2024?

Will the labor market deteriorate and form a feedback loop with consumer spending that leads to a non-linear move in unemployment?

What will happen to the housing market if supply loosens from either lower rates (good) or a softer employment market (bad)?

Where is the tipping point when enough borrowers are forced to refinance at higher rates that there is a material impact to spending?

What is the limit on the fiscal irresponsibility of the US Congress and lenders willingness to condone it?

Will AI speculation drive a historic investment cycle and evolution in how work is done (increased productivity)?

How will the Fed react if the disinflationary trend subsides, and inflation becomes more volatile?

Will the commercial real estate market in the US enter nuclear winter and take regional banks with it?

Will the geopolitical disruptions in Europe and the Middle East spillover to hampering supply chains?

Will the Fed, Congress and the Administration be able to successfully fend off recessionary pressures with programs as the did in 2023?

What will the market reaction be to the US election?