Macro Thoughts

Thought to ponder…

“Ubuntu - how we are and who we are through one another, how our humanity is bound up in one another.”

Dalai Lama, Desmond Tutu, and Douglas Carlton Abrams

The Book of Joy

The View from 30,000 feet

Last week brought important information about the trajectory of the economy over the last quarter, inflation, as well as earnings from the majority of the Magnificent 7. In short, the Fed received no information that could reassure them that it’s time to back away from their hawkish stance – the economy grew at an annualized pace of 4.9% in Q3, well in excess of their projections, and inflation reports came in marginally stronger than expectations. Consumers received troubling news as well. Data showed that personal incomes rose significantly less than spending, resulting in a drawdown in savings, an unsustainable trend. There was no shortage of geopolitical news, which included an expansion of actions in the Israel-Hamas conflict, China opportunistically seizing the distraction in the Middle East to make troubles in the South China Sea, and Trump getting a chance to flex his muscles as the leader of the GOP by helping push forward his candidate for Speaker of the House. As we close out October, investors are hopeful for a Santa Clause rally, and the trend for the last 14 years, where the November-December period ended higher, will continue in 2023. At the same time fresh analysis from Bloomberg Economics is pouring cold water on the party, forecasting a recession that will begin in Q4.

GDP and PCE paint a picture of momentum that supports a hawkish tilt from the Fed, and a strained consumer

Four out of seven of the Magnificent 7 report earnings, and still looking pretty magnificent

Bond shorts starting to throw in the towel and place bets yields will fall in the next 12 to 18 months

The most Frequently Asked Question from clients this week: Why aren’t high rates having a larger impact on the economy?

GDP and PCE - momentum that supports a hawkish tilt from the Fed, and a strained consumer

GDP and economic data releases support hawkish policy.

The first estimate of Q3 GDP was released showing the economy grew at a 4.9% annualized pace in the quarter, ahead of the market survey of 4.5% and well above the Fed’s September Summary of Economic Projections expectation of 2.1%. More troubling is that the Fed believes the economy needs to grow below potential to bring down inflation, which would be somewhere below 1.8%.

S&P Global’s Manufacturing and Services PMI surveys both exceeded expectations and moved into the expansionary zone.

The Chicago Fed National Activity Index, seen as a coincident indicator, indicated that the economy is growing above potential.

The University of Michigan Survey of Inflation expectations 1-yr Ahead surprised higher to 4.2%, from its previous reading of 3.8%

Secretary of the Treasury, and ex-Fed Chair, Yellen in an interview suggested that perhaps the push higher in long-term rates was being driven by growth expectations, which is a less talked about story compared to the current zeitgeist theme of too much supply.

The consumer is digging into savings to support spending amid high inflation and lower trends in wage growth.

Personal Spending increased 0.7% ahead of expectations of 0.5%, while Personal Income increased 0.3%, below expectations of 0.4%. The math is simple – people are increasing their spending faster than their incomes are increasing.

Over the last six months Retails & Food Services Sales have increased at an average pace of 0.6 per month, at an annualize pace of almost 7%. During this same period Personal Savings has dropped from 5.2% to 3.4%.

To support spending, consumers are tapping savings, which comes to a halt if there is any weakness that develops in the labor market. As an important side note, the Fed is specifically targeting cooling the labor market.

The Atlanta Fed Wage Growth Tracker has fallen to 5.2% from 6.4% since March, and is falling slightly faster than Core PCE, which has fallen in the same period to 3.7% from 4.8%. Although it’s a small difference, this signals that wage increases are falling faster than price

The Fed’s quandary – GDP growing well above expectations and disinflationary pressures subsiding

Four of seven of the Magnificent 7 report, and still looking pretty magnificent

Magnificent 7 earnings reports last week:

AMZN $0.83 actual vs $0.81 estimate (2.05% beat)

GOOG $1.55 actual vs $1.45 estimate (7.07% beat)

META $4.39 actual vs $3.70 estimate (18.79% beat)

MSFT $2.99 actual vs $2.66 estimate (12.36% beat)

MTD and YTD performance of Magnificent 7 reporting last week versus the different ways to slice the S&P500 Index:

Investor questions in Q&A on the earnings calls and subsequent market reactions were centered on the potential of cloud businesses to grow and monetize AI tools. Microsoft was seen as a biggest winner on this front because of its early leadership with ChatGPT. Google’s relative underperformance was likely a result of perceptions about its cloud business being relatively smaller and less developed than Microsoft or Amazon.

A more comprehensive look at the S&P500 shows the carnage under the surface, with the equal weight, average and median all solidly negative on the year.

Magnificent 7 labeled as expensive, but not compared to recent, and not so recent, history

Bond shorts starting to throw in the towel and place bets yields will fall in the next 12 to 18 months

Bill Ackman (billionaire hedge fund manager)

Monday, October 23, 2023, from twitter feed - “we covered our bond short…The economy is slowing faster than recent data suggests… There is too much risk in the world to remain short bonds at current long-term rates. ”

Bill Gross (Co-founder of PIMCO and known as The Bond King)

Monday, October 23, 2023, from twitter feed – “Regional bank carnage and recent rise in auto delinquencies to long-term historical highs indicate U.S. economy slowing significantly. Recession in 4th quarter… “Higher for longer” is yesterday’s mantra.”

Bloomberg Economics projects a shallow recession beginning in Q4. Indicators they sited include:

Unsustainable pace of spending growing faster than income

Slowing consumer credit growth and banking willingness to lend

Auto inventories correcting from UAW strike

Slowdown in manufacturing driven by fiscal spending binge winding down

The winter 2022 bears are coming out of hibernation with new arguments tied rates and credit markets

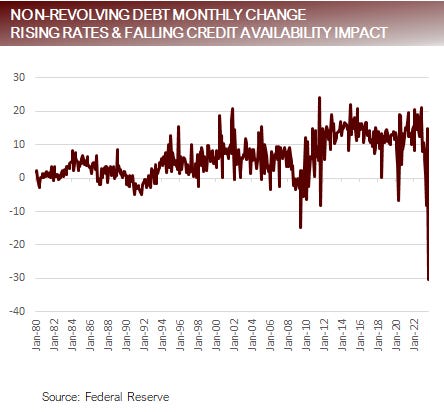

FAQ: Why aren’t high rates having a larger impact on the economy?

Theoretically higher rates should show up first in the “rate sensitive” areas of the economy, which include housing and manufacturing, but also should impact capex spending and capital purchases, but these areas of the economy have been slow to react from higher rates.

The transmission mechanisms to these sectors aren’t working as expected because when the Fed pinned down interest rates to the zero bound between March 2020 and March 2022, consumers and companies had a chance to refinance non-revolving debt and lock in long maturities.

According to RedFin, 82.4% of homeowners have a mortgage rate of less than 5% and 62% have a mortgage rate of less than 4%. In total 99% of borrowers have a mortgage rate of less than 6%.

According the Goldman Sachs, the average interest rate for long-term debt S&P500 companies is currently 3.2%, with only about 8% of the outstanding debt due to mature next year. They don’t see long-term borrowing costs breaching over 4.0% until at least 2025.

Where the rubber hits the road:

If the Fed gets its way and is able to engineer a slowdown the labor market, ie. create job losses, it will likely create forced selling in the housing market and existing home sales will have to find a clearing level, which could be much lower.

It’s estimated that over 40% of Russell 2000 companies have negative cashflow. These companies need to borrow to stay alive. They are zombies. Walking dead. They rely on floating rate instruments and refinancing short-term facilities. As these facilities come due with banks that are facing increased regulatory scrutiny, it will be both expensive and difficult for them to get credit, setting up a potential tsunami of defaults in the small cap sector.

Companies that locked in low rates will be survivors, those that couldn’t will be left for dead

Putting it all together

We’ve called this the “picking up nickels in front of the steam roller market” all year. It’s our view that the fundamental dynamics of a Fed determined to reduce employment and engineer a slowdown don’t support a flourishing economy or stock market, but there are have been various idiosyncratic drivers, such as AI and fiscal stimulus programs that have breathed life into an otherwise dying patient.

With that as the backdrop we continue to see reasons to cautiously take risk. Principally, that the economy seems unlikely to go from 100mph to 0mph in one action. However, we don’t think investors should get married to their positioning because, in the end, we’re going to have the pay the piper, and piper charges a lot of interest these days.

There is an old market adage – what do you call someone who puts on a trade too early? – Wrong. As always, the key will be timing. For this we utilize our quantitative model to help us identify the data turning.

Another way to think about identifying the timing for a slowdown is to qualitatively visualize a cascade of events that leads to the slowdown. One of my recent favorites was published by Andy Constan (https://dampedspring.com/dsr2/), where he lays out what he calls “the Script” – The Only Way to Kill Inflation

Act 1. Higherer for Longerer Island - Hikes continue and don’t achieve goal.

Act 2. Long end yields rise to new highs – Requires a supply catalyst.

Act 3. Multiple compression – Higher yields take the legs out of equity rally.

Act 4. Earnings contraction – The tightening of Act 2 and Act 3 hit demand.

Act 5. Recession Island – Finally. as equities sell off, companies fire workers.