Macro Thoughts

Macro Thoughts

Searching for Signs of "Restrictive" Policy

Thought to ponder…

“Buddhism uses an analogy to describe what happens when we allow fixed beliefs to contour reality for us. Buddhists say that holding such views is like gazing at the sky through a straw. The sky is the unobstructed truth of who we are and what our lives are about. When a received belief system circumscribes that for us, it is as if we are looking at the truth through a narrow tube, seeing only a very small part of it while convinced we are seeing the whole. When we’re attached to our beliefs, we can spend a lot of time comparing straws: “I’ve got a better straw than you. It’s a little wider and it’s got a design on it.” Especially in the face of fear, we tend to hold on to our straws with a death grip.. “

Sharon Salzberg

Faith

The View from 30,000 feet

Last week started out with a shockwave and ended with a bang. The shockwave was caused by the ISM Services release which confirmed the Manufacturing survey of the previous week, indicating a sharp spike in the Price Paid component, which sealed the deal for the consensus to shift expectations away from a rate cut in March. The bang was when the S&P500 breached 5,000 for the first time. Although from a mathematical perspective there’s nothing special about 5,000, what was perhaps more interesting was another round number we sailed through – the forward price to earnings ratio for the S&P500 moved above 20. Apart from the parabolic liquidity driven rally immediately following the pandemic, the market is now the most expensive it’s been since the early 2000’s. The other interesting development last week was the flood of strategists, pushing their Q1 2024 and full year 2024 GDP projections higher. Since bottoming last July at 0.6%, the Bloomberg survey of economists for 2024 GDP has been a steady marching higher. The last official reading was in January, when the consensus estimates was for a 1.5% annual rate of growth in 2024. With the Atlanta Fed’s GDPNow most recent estimate projecting the annualized growth rate for Q1 to be 3.4%, and the economy appearing to be accelerating, in spite of what’s been labeled “restrictive” interest rate policy, both the Fed and private sector economists are now having to rethink their projections and perhaps even their definition of “restrictive”.

Why the Fed needs more evidence that disinflationary trends will continue

Searching for evidence of rates being restrictive

Earnings Dashboard Update: Margins driving performance

Refreshing the probabilities of market outcomes for 2024 (updates from Outlook provided in November 2023)

Focus Point Sector Rotation Update

Why the Fed needs more evidence that disinflationary trends will continue

If there was on word that resonated as a takeaway from Fed pressor on January 31st it was “confidence”, or more specifically, a lack thereof. The 25-page transcript of the press conference was littered with the word “confidence”, which Powell uttered by Powell 31 times in reference to the Federal Reserve needing to have more of it to believe inflation was under control. This sentiment has been emphasized in unison by a marching band of Fed Presidents since the FOMC meeting.

In a variety of venues over the last quarter the Fed outlined three forces leading to the disinflationary pressures of 2023:

Easing of supply chain pressures

Resurgence of workers into the workplace increasing participation

Lower energy prices

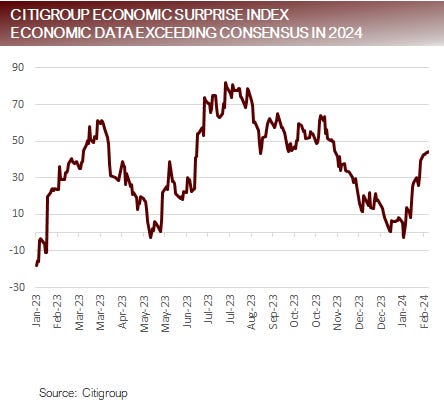

The aggregation of this information was reflected in the Citigroup Inflation Surprise Index, which has fallen precipitously

The last shoe to drop for the disinflationary process to maintain momentum is housing, but with housing prices showing signs of stabilizing, and demand beginning to pick up as mortgage rates have fallen about 100 basis points from their peak, it’s not clear the degree to which housing will contribute to the disinflationary cause in 2024.

Checking in on how the factors that drove disinflation in 2023 are moving in 2024:

The New York Fed Global Supply Chain Pressure Index has been trending consistently higher since June 2023

The Prime Age Labor Participation Rate (24 to 55 year olds) has been trending down since October 2023

Brent Crude is up 6.3% since the beginning of the year

The Citigroup Inflation Surprise Index bottomed in July 2023 and has begun trending higher

Supply chains and labor participation have normalized and won’t contribute as much in 2024

Searching for evidence of rates being restrictive

Fed Funds increased 525 basis points between March of 2022 and July of 2023, prompting the Federal Reserve to include the following statement in the FOMC Statement.

“Over the past two years, we have significantly tightened the stance of monetary policy. Our strong actions have moved our policy rate well into restrictive territory, and we have been seeing the effects on economic activity and inflation.”

Taking a look at some measures that would indicate that rates are restrictive provides some interesting counterpoints to this statement:

New Vehicle Sales, have increased from an annual run rate of 13.3m in March of 2022 to 15.0m in January of 2024

The latest GDP release shows a continued trend of Residential Fixed Investment increasing the last two quarters

Last week’s New York Fed Senior Loan Officer Survey indicated a resurgence in both loan supply and loan demand

GDP was growing at an annualized rate of 3.6% at the end of March 2022, and as of the most recent report is growing at 3.1%. To put this in context, the average annualized growth rate between 2011 and 2019 was 2.3%.

There has been increasing interest in the topic of the neutral rate of interest, with more and more commentary suggesting that perhaps the neutral rate of interest is higher than prior to the pandemic, when it was thought to be between 2.0% and 2.5%. If the neutral rate has indeed moved higher, expectations for the floor for interest rates may need to be adjusted.

If interest rates are restrictive, wouldn’t we expect tighter lending standards and less demand?

Earnings Dashboard Update: Margins driving performance

With 67% of the companies in the S&P500 having reported Q4 earnings, the number beating earnings and revenue estimates are now above historical averages.

One of the stories of Q4 is margins. The two sectors to grow margins most over the last year have been Communication Services and Information Technology. It’s no coincidence that these are the two best performing sectors of the S&P500 in 2024, up 7.98% and 8.96%, respectively, year to date.

Another big story of the quarter is valuation. The S&P500 is now trading at 20.3x its forward price to earning ratio. Only two sectors are trading richer than the average: Information Technology and Consumer Discretionary. Interestingly, Consumer Discretionary is only up 0.61% year to date, indicating the investors may be struggling to accept the valuation in this sector.

Valuations providing less margin of safety for disappointments in 2024

Refreshing the probabilities of market outcomes for 2024 (updates from November 2023)

Upside in equity market being driven by a mismatch of economic expectations for 2024

Focus Point Sector Rotation Update

The Focus Point Sector Rotation Model is a combined trend following and mean reversion model that utilizes seven factors to analyze daily price data on sectors to determine the strength of upward trends.

Most interesting move of the week was the slight weakening of the upward trend in Comm Services, which has led the rally in 2024. Further deterioration in this sector would challenge upside momentum in the broad market.

Putting it all together

Early 2024 is shaping up similarly to 2023 with some key differences:

Similarities

Economist and strategists entered the year too bearish

Leadership is concentrated in the top names

The mismatch of low expectations and better than expected results has provided an upside lift to equities

Differences

A healthy does of humility from the action of eating hat has made most economists and strategists quicker to revise their estimates higher

Most of the Magnificent 7 remain leaders but new entrants such as Broadcom are trying to fight their way into the fold

The outlook for inflation and interest rates is much different in February 2024 from February of 2023

Valuations have spiked to the highest levels in two years

The larger picture is that the economy is humming along faster than the Fed or strategists had expected, which has manifested in a stronger job market than anticipated and resilient spending. At the same time, disinflationary momentum has continued, but there are some questions as to if the last mile of disinflation will prove to be an easy road. With valuations skyrocketing, expectations that rate cuts are just around the corner, geopolitical turmoil making daily headlines and regional banks back in the spotlight, the markets are climbing a wall of worry that may lead to volatility.