Macro Thoughts

Thought to ponder…

“After each storm, we become stronger, more solid, and soon we’re no longer fearful of storms. We no longer pray for a calm sky and a calm ocean. Instead, we pray that we have the wisdom and strength to deal with the difficulties that arise in life.

Thich Nhat Hanh

Happiness

The View from 30,000 feet

The doves lined up last week guiding the S&P500 up 5.85%, marking the best week of performance for the year. A busy week of data began with the quarterly refunding announcement from the Treasury. After being shell shocked by the magnitude of the July announcement, nervous investors instead had a chance to take a deep breath when the announcement came in slightly lighter than market expectations. The good news continued with positive surprises on Productivity and Unit Labor Costs, a new and improved Powell, who was beaming with confidence, weaving a story of falling inflation matched with cooling employment, and subtly backing away from intentions to hike further. Towards the end of the week claims data reinforced a picture of a more difficult labor market, which was followed by a payroll reports that was in two words – not good. For the markets bad news was good news, and by the end of the week equities were higher, Fed Funds Futures had moved from pricing in three cuts next year to four, Treasury yields began to plummet and financial conditions had loosened significantly with equities continuing to do what they’ve done since July – follow the Treasury market around like a stars truck lover. Not even lackluster comments from Apple were enough to dissuade buyers. Now the big question is – will the rally stick and gel into the consensus Q4 boom expected, or will it fade as bad news actually becomes bad news?

Powell transitions from careful to confident, with the first subtle hints of taking a victory lap

Employment data begins to show signs of deterioration, now the worry become non-linearity

The first hints of Q4 earnings and data indicate expectations for growth should be tempered

The most Frequently Asked Question from clients this week: Is the market rally sustainable?

Powell transitions from careful to confident, with the first subtle hints of taking a victory lap

The language from FOMC statement had nuanced signs of acknowledging improving conditions. The assessment of the economy was described as “strong” instead of “solid” and employment was described as “moderated” instead of “slowed”.

Powell had a sense of confidence that, in my opinion, we haven’t seen him display before. The he seemed confident that the Fed had raised rates to restrictive level, but left open that they weren’t sure they are currently restrictive enough. Sounded like a victory lap to me. Paul Krugman, the Nobel winning economist, declared the war against inflation has been won.

He hammered home the point that the Committee is not thinking or talking about cutting rates, they are focused on two questions:

Are they high enough (restrictive enough) to bring down inflation to their target?

How long will they have to keep rates high to gain confidence that inflation is on a trajectory to their target?

There were a lot of questions about if tightening financial conditions are doing some of the work for the Fed. His response was to acknowledge that the Fed is currently getting help from tighter financial conditions but for it to be helpful the tightening of financial conditions would need to be persistent.

The markets took Powell’s responses as proof positive that the Fed is done for the cycle, setting off a rally that soft jobs data poured fire on later in the week. The irony is that the falling rates, and rising equity market, both feed into loosening of financial conditions, which goes contra to what the Fed needs to see to stay dovish.

Financial conditions not persistent and loan growth still moving higher – Keeps Fed vigilant

Employment data begins to show signs of deterioration, now the worry become non-linearity

Job openings were uneventful. The current monthly report beat slightly, while the past month was revised lower by a similar magnitude. Stronger trends in demand were observed in Construction, Manufacturing and Leisure / Hospitality, while weaker trends in demand were observed in Information Tech and Government. With only 31% of those sent surveys bothering to respond, trends are important, but the actual numbers may not reflect reality.

ISM survey employment was eventful. Both Manufacturing and Services posted surprising large hits versus expectations to the employment component of the survey.

Jobless claims data was eventful. Continuing Claims have begun to move up sharply, which may signal employers are not yet cutting employees, but hiring has slowed, so those who are unemployed are having a more difficult time finding work.

The Payroll Report was packed full of events. With the recent uptick in claims data and unemployment approaching the Sahm rule, key will be seeing if the Fed can gently land employment which has a habit of non-linear patterns.

Nonfarm Payrolls (establishment survey) missed to the downside by a wide margin, printing 150k vs. 180k expected, with the previous period revised lower. However, by definition the establishment survey includes only people who receive pay for the reference period, so the UAW strike added a lot of noise to this number.

The Unemployment Rate (household survey) missed to the downside with the Unemployment Rate rising to 3.9% from 3.8%. This is significant because it puts the Unemployment Rate with striking distance to the Sahm Rule, which is the reference point where the three-month moving average of the Unemployment Rate is within half a percent of its 12-month low, and historically has coincided with the beginning of a recession. It should be noted, even Claudia Sahm, who invented the indicator is skeptical that the rule will be accurate this time around

Claims data hooking higher and first measure of labor cost returns to pre-pandemic levels

The first hints of Q4 earnings and data indicate expectations for growth should be tempered

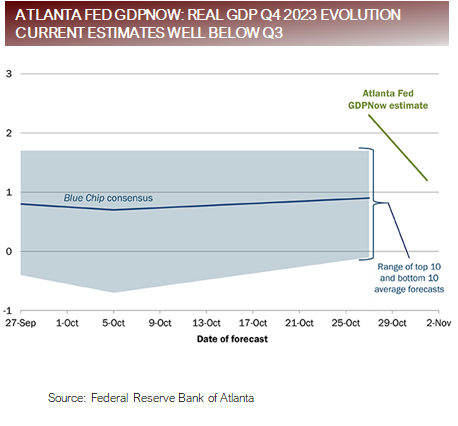

At the end of October the Atlanta Fed GDPNow was the talk of the down because it was indicating near 5% GDP growth for Q3. The same model has now given the first two weekly reading for Q4, where it began projecting 2.3% and has now fallen to 1.2%.

Two other Federal Reserve banks produce GDP Forecasts.

Federal Reserve of New York GDP Nowcast: 2.41%

Federal Reserve of St. Louis GDP Nowcast: 2.31%

At this point in the quarter the error bands are wide because now cast models are only projecting based on data reported in the quarter. With two months left to go, there are a lot more data. However, one thing seems likely so far, the pace of growth seen in Q3 is unlikely to repeat.

With 81% of S&P500 companies having reported, we’re starting to get a read on Q4. Two observations come to mind in looking at the data, companies are lowering guidance in Q4, and companies that miss guidance are being severely punished.

The Good News

82% of companies in the S&P500 have reported earnings above their estimates, which is above both the 5 and 10-year averages.

The average earnings beat has been 7.1%, which is below the 5-year average of 8.5%, but above the 10-year average of 6.6%

The Bad News

Analysts have lowered Q4 earning estimates by 3.9%, which is over twice what’s normally been seen over periods of 5, 10, and 20 years.

The average move to the downside of companies missing estimates (looking two days before to two days after earrings release) has been -5.2%, which is over twice the downside over the last 5-years.

Source: Factset

Momentum in GDP slowing coming into Q4 and markets are nervous of misses

FAQ: Is the market rally sustainable?

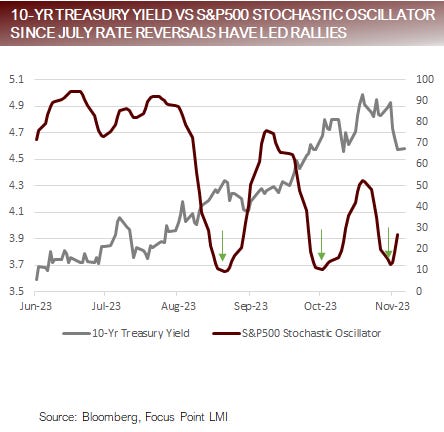

The equity markets have been following the lead of interest rates since July – as interest have rates moved higher, equities have been pressured.

Over the last week, quarterly refunding, comments from the Fed, and weak labor numbers have combined to create a situation where the markets are again beginning to price in an increasing number of rate cuts in 2024.

We have to ask the question, what would cause interest rates to come down faster? The answer is tied to economic weakness, either showing up in GDP, labor or both.

The next question would be what does this mean for earnings, and consequently the equity markets? If you’re inclined to believe that equity prices reflect earnings this could be troublesome. Currently, according to Factset S&P500 2024 Earnings are projected to be $246.39, which represents 11.4% earnings growth over 2023. This would be above the long-term average of 6% to 8% a year. This means that S&P500 is projected to grow at roughly twice the average pace next year while rates are the most restrictive they’ve been since 2007. This seems like a stretch.

The equity markets were oversold, and the 10-year failed to on multiple attempts at breaching 5.0%. We’re fresh off a week were pretty much everything went right to limit further upside in yields, and it showed up in market action. This led to a relief rally in equities, tied to short covering, optimism that the Fed is done and people chasing a yearend Santa Claus rally. It’s hard to tell how much follow through will be behind this, but it doesn’t seem to be a fundamental move if what we’re seeing companies and analysts lowering earnings expectations, GDP forecasts falling and labor cooling off.

Bottom line, it’s too early to tell if the rally will have legs and if it does to what level, but if it does continue, the bigger question is will this be the last nickel to be picked up before the steam roller moves in for the kill?

Last week’s market rally driven by rates move lower, for the rally to stick rates need to stall

Putting it all together

The fall in equity prices in Q3 was driven by the steady rise in yields. With Powell signaling the hiking cycle may be done, and the first readings on Q4 GDP and employment data coming in generally weaker than expected, it appears that the ceiling on rates may be in unless growth data employment, start to signal more resilience. The equity market’s manic reactions to yields and each print of economic data highlights the data dependency stage the Fed has set, where each economic release generates euphoric reactions of joy or fits of terror and despondence.

This leaves some questions for the equity markets. If the late summer/fall selloff was driven by rising rates, is it reasonable to expect a ceiling in rates will create (i) a sizeable rally, (ii) a consolidation or (iii) a continuation of the downtrend? If the ceiling in rates is a result of poor economic data, it may well lead to weaker earnings. It’s hard to make a case for significantly higher prices in equities with poor data and falling earnings. It’s also hard to make a case for a resumption of the downtrend until information substantiates that the bad news is so bad that it’s actually bad news for earnings, which hasn’t happened yet.

This means that market are likely caught in a trading range. Now that the data appears to have begun deteriorating, we’ll need to see the glide path of the deterioration to determine if the markets can deliver on 2024 earnings expectations in spite of not so bad economic news, which could signal upside, or will the economy be overcome by the traditional negative feedback loops that are typically observed with material slowdowns.