Macro Thoughts

Thought to ponder…

“We don’t have the power to choose all of our experiences, but we always have the ability to choose our behavior in the midst of them and in their wake, and those choices are what define our character.

Greg Everett

Tough

The View from 30,000 feet

A week ago, we commented in Macro Thoughts to expect more volatility in March because, with earning season drawing to a close, there would be less availability of corporate news, so the markets were likely to trade with increased attention on data releases and politics. Last week did not disappoint. The average intraday range of the S&P500 last week was 0.88%, which compares the average since the start of the year of 0.76%. The week was loaded with trigger points, including a full Fed speaking calendar and Powell’s semiannual testimony to Congress, where Powell reassured Fed watchers that the Fed would be cutting interest rates “at some point in 2024” and the Fed is “not far” from having confidence that inflation is on a trajectory to 2% that would usher in the beginning of an easing cycle. Biden’s State of the Union speech kicked off the rematch between Biden and Trump. The next nine months promises to provide a lot of fireworks with the Wall Street Journal describing the difference between the two candidates’ views as those of “A resurgent America making steady progress toward a future of shared prosperity” versus “a dystopian backwater on a path to ruin.” It was labor week, with data on job openings, unemployment claims, hiring and unemployment. The net result of the data was a continuation of the view that the labor market is tightening and moving towards the Fed’s projections. Next week will be particularly interesting with CPI on Tuesday. Last month’s CPI came in hot. This month will hold special importance because now that the labor market is confirming signs of weakening, if CPI continues to run above estimates, the Fed will be stuck between rock and hard place, where the economy is growing, inflation is persistent, and the employment market is softening, not what they’re looking for.

Labor Dashboard: Unemployment rate finally confirms cooling in the labor markets

Global Purchasing Manager Indexes (PMIs) showed signs of an improving global manufacturing economy vs. Institute of Supply Management (ISM) US-centric view which signaled softening

Broadening out of the markets fait accompli – eleven out of eleven sectors now up on the year

Focus Point Sector Rotation Update: Fading 2023 leadership

Labor Dashboard: Unemployment rate finally confirms cooling in the labor markets

After months of deteriorating data, the unemployment rate finally hooked higher, reaching its highest level since January 2022.

Although the change in nonfarm payrolls came in higher than 75 out of 76 of the Bloomberg survey estimates, the market impact was muted due to heavy downward revisions of prior months.

The quits rate fell to levels not seen since 2017, indicating that workers may be getting nervous about leaving their jobs.

NFIB Hiring Plans continue to fall, while a lower percentage of companies surveyed by NFIB are finding Jobs Hard to Fill.

There is a clear downtrend in ISM Manufacturing and Services Employment component.

The majority of employment indicators are falling, with questions looming on reliability of data

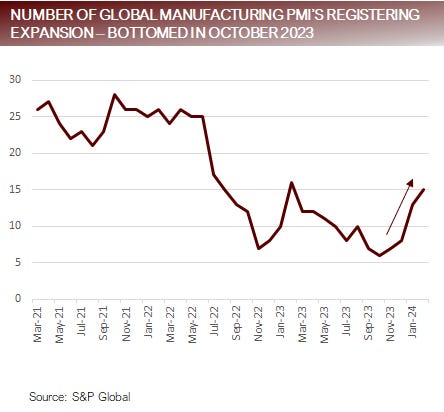

Global PMIs improving global economy vs. ISM in the US, not so much

Global Manufacturing PMIs are improving.

4 out of 5 of American PMIs are improving, with Columbia being the sole outlier, that continues to deteriorate.

12 out of 13 of European PMIs are improving, with Germany being the sole outlier, that continues to deteriorate.

6 out of 12 of the Asian PMIs are improving, suggesting a mixed bag in Asia.

Global Manufacturing PMIs bottomed in October, with only 6 out of 30 countries in expansion, and have since improved to 15 out of 30 countries in expansion.

Global Services PMIs are a mixed bag with 7 out of 13 PMIs improving.

US Institute of Supply Management Surveys are deteriorating. The brief uptick in January has dissipated and the leading indicators are softening. The weakness is particularly evident in the manufacturing data.

Global Manufacturing sectors showing revival, with strength centered in Europe

Broadening out of the markets fait accompli – eleven out of eleven sectors now up on the year

At the end of January 4 out of 11 sectors in the S&P500 were up for the year. By the end of February 9 out of 11 sectors were up for the year. As of last the close on Friday, 11 out of 11 sectors were up on the year.

The broadening out also includes international markets. Last week the MSCI EAFE Index, which measures developed global equity markets outside the US, outperformed the S&P500 by 260 basis points, which was the 8th largest gap in outperformance over the S&P500 in the last 120 weeks, with only one week in 2023 being better.

The S&P500 was up 7.72% as of the close Friday, with 38% of the companies in the S&P500 outperforming the index, which compares favorably to the end of January when only 28% of the companies were outperforming the index. However, this still falls short of the 10-years prior to the pandemic when about 49% of the companies within the index outperformed the index.

The Magnificent 7 has fallen apart in 2024, with Nvidia and Meta remaining top dogs driving the index and the other 5 nowhere to be found. In fact, Nvidia is the best performing company in the S&P500 this year, up a staggering +76.8%, while the worst performing company in the index, another familiar Mag 7 name, Tesla, which is down -29.4% for the year.

Nvidia and Meta together account for 64% of the gain in the S&P500 this year. The top 10 largest companies together account for 82% of the gain in the S&P500 for the year.

Since the beginning of March, Defensives have outperformed Cyclicals by 104 basis points. Only two months in 2023, did Defensives outperform Cyclicals by more, which were September, the worst month of 2023 and April, the month after SVB blew up.

Cyclical vs Defensive performance – March a winner for cyclicals, but they are still a laggard

Focus Point Sector Rotation Update: Fading 2023 leadership

The Focus Point Sector Rotation Model is a combined trend following and mean reversion model that utilizes seven factors to analyze daily price data on sectors to determine the strength of upward trends.

The trends broadened out with 10 out of 11 sectors in uptrends.

The two closest sectors to failing their uptrends are Comm Services and Info Tech.

Good news from a breadth standpoint, falls under the careful what you wish for header, because Comm Services and Info Tech make up 39% of the S&P500, and without them it will be difficult for the index to gain meaningful ground.

Putting it all together

In the larger picture, the messaging from the Fed is unchanged – they expect 2024 to be the year that they begin rate cuts. Expectations surrounding the timing and number of cuts varies from economic print to economic print and from Fed President speech to Fed President speech. The markets will remain volatile around data releases and Fed speeches.

The election campaigning kicked off in earnest last week. The two parties have dramatically different viewpoints of the state of the Union. This too will generate volatility speeches depending.

The market are in the dead zone between reporting seasons for the next four weeks. In markets with light corporate earnings news, between reporting seasons, the markets are susceptible to increased volatility because things other than company driven news can grab headlines and more easily sway investor sentiment.

The most recent Atlanta Fed GDPNow is measuring economic activity in Q1 at 2.5%, above trend. Progress on disinflationary trends have stalled, and hinge on what happens with housing (owners equivalent rent) and wages.

Stronger than expected economic activity combined with stalled inflation could be a bad tasting cocktail for the markets because the Fed may be hesitant to cut rates into this environment. However cooling labor markets may signal the Fed should start cutting soon. If these trends continue, it puts the Fed in quandary, where they may be damned if they do and damned if they don’t’.